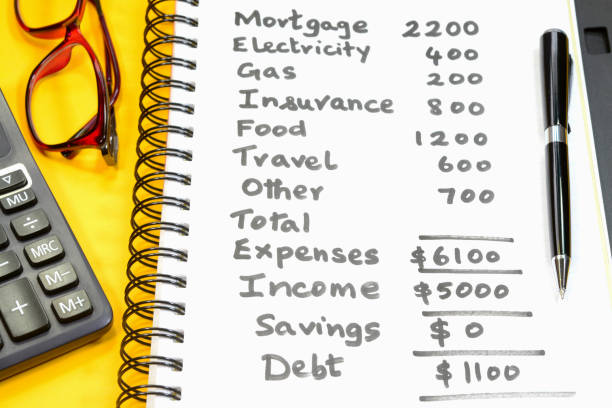

The burden of overextended personal debt is more than a financial condition; it is a state of being that can feel inescapable. When monthly obligation...

Read More

Entering one’s twenties often marks the beginning of true financial independence, a period of exciting possibilities juxtaposed with significant eco...

Read More

In the landscape of personal finance, few situations are as precarious as being overextended by debt. This state, where a significant portion of one's...

Read More

The peril of overextended personal debt is often not a sudden plunge into financial chaos but a gradual, almost imperceptible descent fueled by a phen...

Read More

The most effective strategy for managing overextended personal debt is to prevent it from occurring in the first place. This requires a shift in finan...

Read More

The burden of student loan debt represents a uniquely formidable contributor to the crisis of overextension, particularly for individuals in their pri...

Read More

Conduct a thorough spending audit. Cancel unused subscriptions, reduce dining out, negotiate lower bills (like insurance or phone plans), and temporarily halt discretionary spending on non-essentials.

Yes. The definition of overextension is not just about defaulting; it's about a lack of financial resilience. If an unexpected $500 expense would force you to miss a payment or take on more debt, you are likely overextended and living paycheck-to-paycheck.

Monitor credit reports closely, remove authorized user statuses, freeze joint accounts, and ensure all divorce-mandated payments are made on time to avoid negative marks.

Ceasing payments will lead to late fees, increased interest rates, and aggressive collection efforts, including lawsuits and potential wage garnishment. Creditors are not obligated to negotiate, and this strategy can significantly increase the total amount owed due to penalties.

Yes. Paying at least the minimum payment by the due date will keep your account in good standing and prevent negative marks on your credit report. However, paying only the minimum will extend the life of your debt and cost you significantly more in interest.