In the bleak landscape of overextended personal debt, non-profit debt relief agencies emerge as a critical beacon of hope and pragmatism. Unlike their...

Read More

Navigating the labyrinth of healthcare debt requires a unique blend of financial strategy and systemic understanding, distinct from managing other for...

Read More

The reality of overextended personal debt is a landscape of profound anxiety, where monthly obligations eclipse income and the future feels foreclosed...

Read More

The desperate landscape of overextended personal debt has given rise to a controversial industry that purports to offer a lifeline: for-profit debt re...

Read More

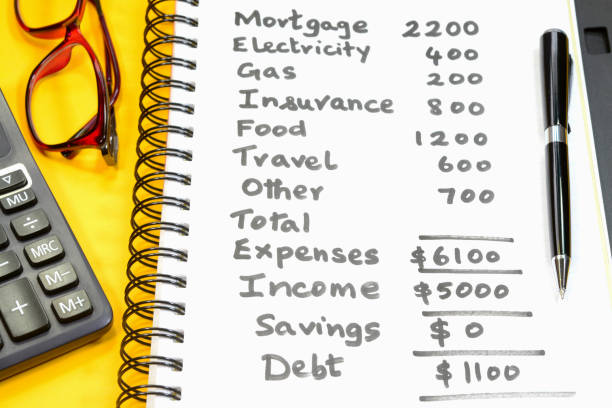

Are you managing your debt? Or is it managing you? If you're stuck in a money quicksand trap, you may not even realize at first that you're in a finan...

Read More

- Start by taking inventory of all your outstanding debts. - Look for ways to maximize your disposable income so you can put more money towards your ...

Read More

If the information is incorrect (wrong amount, wrong date, etc.), you can file a dispute directly with the credit bureau reporting it. They are required to investigate and correct verified inaccuracies.

Yes, many credit card issuers have well-established hardship programs where they may temporarily lower your APR to as low as 0% for a set period, making payments more manageable and helping you pay down the principal faster.

When housing costs exceed a third of a person's income, it forces difficult trade-offs. Essentials like food, transportation, and healthcare may be sacrificed or put on credit, creating a cycle of debt just to afford basic shelter.

The desire to maintain a certain social status or keep up with peers' spending on homes, cars, and vacations can lead to financing a lifestyle beyond one's means, often using debt to fund the appearance of success.

Every dollar spent on interest payments for emergency debt is a dollar not invested for retirement, saved for a home, or spent on enriching experiences. It actively undermines future wealth building and financial security.