The relationship between overextended personal debt and a medical crisis represents one of the most devastating and morally fraught intersections in m...

Read More

The burden of overextended personal debt takes on a uniquely cruel dimension when its primary source is medical expense. Unlike debt accrued from disc...

Read More

Entering one’s twenties often marks the beginning of true financial independence, a period of exciting possibilities juxtaposed with significant eco...

Read More

Navigating the labyrinth of healthcare debt requires a unique blend of financial strategy and systemic understanding, distinct from managing other for...

Read More

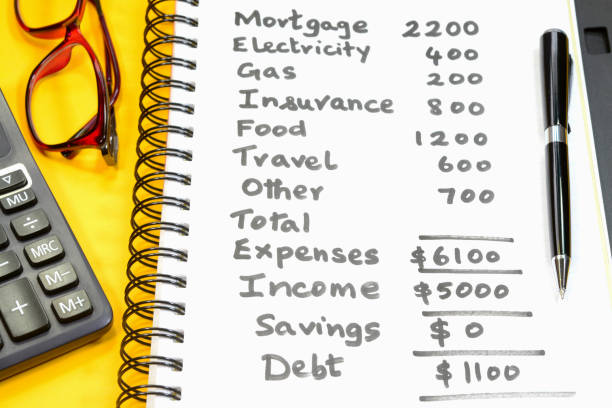

In the landscape of personal finance, few situations are as precarious as being overextended by debt. This state, where a significant portion of one's...

Read More

The phenomenon of overextended debt is often mischaracterized as a simple failure of mathematical calculation or fiscal discipline. However, behaviora...

Read More

A good rule of thumb is to keep your overall ratio below 30%. For the best possible credit score, experts recommend maintaining a ratio in the single digits (below 10%).

Some providers may accept a reduced lump-sum payment to settle a debt, especially if you’re experiencing financial hardship. Always request this in writing.

This final 10% factor looks at how many new accounts you've recently opened and the number of hard inquiries on your report. Applying for several new lines of credit in a short period is seen as risky behavior and can indicate financial stress, leading to a score decrease.

This is when you return the car to the lender because you can no longer make payments. It severely damages your credit score and does not relieve you of the debt; you will still owe the difference between the loan balance and what the car sells for at auction.

Individuals may not know methods like the debt avalanche (paying high-interest debt first) or snowball (paying small balances first) methods, so they pay debts inefficiently, costing more time and money.