The relationship between overextended personal debt and conspicuous consumption is a modern tragedy, where the pursuit of social validation through material display leads directly to financial peril. This dynamic, first articulated by economist Thorstein Veblen, describes consumption aimed at signaling status and wealth rather than fulfilling practical needs. In today’s economy, fueled by social media and readily available credit, this pursuit has become democratized and dangerously accessible, allowing individuals to finance an illusion of prosperity they cannot genuinely afford.The mechanism is seductively simple. Credit cards, “buy now, pay later” plans, and auto loans provide the immediate means to acquire status symbols—the luxury vehicle, the designer handbag, the lavish vacation—without the immediate financial pain. This disconnect between purchase and payment creates a psychological illusion of affordability, encouraging spending that far exceeds one’s actual income. The act of acquisition provides a short-term dopamine rush and a public marker of success, but it is built on a foundation of future obligations. The curated perfection of online life exacerbates this, creating relentless pressure to keep up with a perceived standard of living, real or fabricated by others.The consequence, however, is a harsh and inescapable reality. The monthly statements arrive long after the social media likes have faded, revealing the true cost of that illusion. Minimum payments create a suffocating cycle of compound interest, where the debtor finds themselves working not to get ahead, but merely to service the interest on the lifestyle they have already consumed. Savings become impossible, and financial resilience evaporates. An unexpected job loss or medical bill can instantly collapse the entire fragile facade.Ultimately, conspicuous consumption financed by debt is a Faustian bargain. It trades long-term security for short-term social currency, leveraging one’s future to purchase status in the present. The material goods acquired inevitably depreciate, lose their novelty, or are replaced by newer trends, but the debt remains, growing and persistent. This leaves the individual not with enhanced social standing, but with anxiety, regret, and a profoundly compromised financial future. The pursuit of appearing wealthy becomes the very obstacle to ever becoming so, revealing a painful irony: the most conspicuous thing often being financed is not the luxury item itself, but the devastating debt required to own it.

The relationship between overextended personal debt and conspicuous consumption is a modern tragedy, where the pursuit of social validation through material display leads directly to financial peril. This dynamic, first articulated by economist Thorstein Veblen, describes consumption aimed at signaling status and wealth rather than fulfilling practical needs. In today’s economy, fueled by social media and readily available credit, this pursuit has become democratized and dangerously accessible, allowing individuals to finance an illusion of prosperity they cannot genuinely afford.The mechanism is seductively simple. Credit cards, “buy now, pay later” plans, and auto loans provide the immediate means to acquire status symbols—the luxury vehicle, the designer handbag, the lavish vacation—without the immediate financial pain. This disconnect between purchase and payment creates a psychological illusion of affordability, encouraging spending that far exceeds one’s actual income. The act of acquisition provides a short-term dopamine rush and a public marker of success, but it is built on a foundation of future obligations. The curated perfection of online life exacerbates this, creating relentless pressure to keep up with a perceived standard of living, real or fabricated by others.The consequence, however, is a harsh and inescapable reality. The monthly statements arrive long after the social media likes have faded, revealing the true cost of that illusion. Minimum payments create a suffocating cycle of compound interest, where the debtor finds themselves working not to get ahead, but merely to service the interest on the lifestyle they have already consumed. Savings become impossible, and financial resilience evaporates. An unexpected job loss or medical bill can instantly collapse the entire fragile facade.Ultimately, conspicuous consumption financed by debt is a Faustian bargain. It trades long-term security for short-term social currency, leveraging one’s future to purchase status in the present. The material goods acquired inevitably depreciate, lose their novelty, or are replaced by newer trends, but the debt remains, growing and persistent. This leaves the individual not with enhanced social standing, but with anxiety, regret, and a profoundly compromised financial future. The pursuit of appearing wealthy becomes the very obstacle to ever becoming so, revealing a painful irony: the most conspicuous thing often being financed is not the luxury item itself, but the devastating debt required to own it.

Choosing the wrong card can deepen debt through high fees and interest, while the right card can be a strategic tool for reducing costs and managing payments more effectively.

This is when you return the car to the lender because you can no longer make payments. It severely damages your credit score and does not relieve you of the debt; you will still owe the difference between the loan balance and what the car sells for at auction.

Look for issuers that offer free credit score tracking, spending alerts, and easy-to-use mobile apps. These tools can help you monitor your progress and stay on budget.

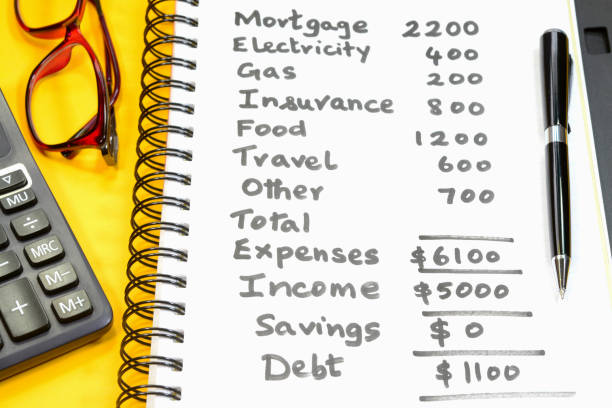

Plan for known expenses (childcare, education) and build a robust emergency fund (3-6 months of expenses) to cover unexpected costs. This prevents you from reaching for credit cards when surprises happen.

Focus on: Account Balances and Credit Limits (to calculate utilization), Payment History (for any missed payments), Account Status (for charge-offs or collections), and Credit Inquiries (to see who has recently accessed your report).